What happens when your favorite DeFi protocol gets hacked or your stablecoin drops below peg? These risks are real, and more users are now looking for protection they can trust.

That’s where the search for the best decentralised insurance project begins. It’s not just about avoiding losses. It’s about building safer systems that support the future of Web3.

This article breaks down what decentralised insurance really is, why it matters in today’s crypto landscape, and how to evaluate the top platforms in 2025.

You’ll get a full look at the leading projects, emerging players to watch, real use cases, and the challenges still holding the space back. Whether you’re deep in DeFi or just starting out, this article will help you understand how to choose the right protection for your crypto assets.

Key Takeaways

- Decentralised insurance protects crypto users from risks like hacks, bugs, and stablecoin depegs.

- It uses smart contracts and pooled capital to automate coverage and payouts.

- Platforms like Nexus Mutual and InsurAce lead the space with proven claim records.

- DAOs and DeFi protocols are starting to insure their own treasuries on-chain.

- The best decentralised insurance project balances fair pricing, strong liquidity, and reliable claims.

What Is Decentralized Insurance?

Decentralized insurance is a new way of providing coverage using blockchain technology instead of traditional insurance companies. It works through smart contracts, which are self-executing programs that run on blockchains like Ethereum.

These contracts automatically handle things like policy creation, premium collection, and claim payouts based on predefined conditions. This setup removes the need for middlemen and lets people access insurance directly through a decentralized network.

Most decentralized insurance protocols are governed by their communities through DAOs where token holders vote on decisions, including whether to approve claims. The goal is to make insurance more open, efficient, and accessible to anyone with an internet connection.

For example, if someone uses a DeFi protocol like Aave or Curve, they can buy decentralized insurance to protect their funds in case of a smart contract hack. A project like Nexus Mutual offers this kind of coverage. When an incident happens, members of the mutual review it and vote on whether to approve a payout.

Other platforms like Risk Harbor automate this process entirely using data and logic to determine whether a claim is valid. This model is becoming more popular as people look for ways to protect their digital assets without relying on banks or centralized institutions.

“DeFi hacks caused over $3 billion in losses in 2022”

Top Decentralized Insurance Projects (2025)

If you’re looking for trusted options, here are the decentralized insurance platforms worth knowing right now.

1. Nexus Mutual

Nexus Mutual launched in 2019 as the first decentralized insurance mutual built on Ethereum. It lets users join as members through KYC, stake NXM tokens, and share risks across smart contracts, custody, and protocol failures.

Pros:

- Community-led governance ensures transparency.

- Broad coverage for smart contracts, exchanges, and custody.

- Real-world track record with over $18 million in payouts.

- Strong on-chain audits and risk assessment.

- Capital pool backed by staking, aligning incentives.

Cons

- Requires KYC, which can limit participation.

- Claims decisions can be slow or politicized.

- NXM token value impacts premiums and coverage cost.

- Exposure is largely restricted to the Ethereum ecosystem.

- It can be complex for newcomers to navigate.

2. InsurAce

InsurAce started in 2021 as a multi-chain insurance DAO offering over 100 cover options. It includes protocol, stablecoin depeg, and custodian protection, with capital crowdsourced across Ethereum, BSC, Polygon, and Avalanche.

Pros

- Multi-chain support reduces gas costs and extends reach.

- Dynamic pricing is tied to supply and demand.

- Claims vetted by an expert board plus community input.

- No KYC requirement.

- Offers staking rewards and yield opportunities.

Cons

- Payouts can take 7–30 days, which may frustrate users.

- The interface and product range can overwhelm beginners.

- Smaller capital reserves than older platforms.

- Trust is still building relative to Nexus.

- Manual claim steps may slow the process.

3. Tidal Finance

(Source: Tidal Finance website)

Tidal Finance operates as a cross-chain insurance aggregator using capital-efficient, customizable pools. Liquidity providers underwrite coverage and earn premiums through TIDAL tokens.

Pros

- High capital efficiency via targeted coverage pools.

- Flexible terms let providers choose risks.

- Fast payouts and increased composability.

- Competitive premiums based on coverage specifics.

- Rewards encourage active liquidity provision.

Cons

- Less proven due to its relative youth.

- Liquidity quality varies by pool.

- Risk depends heavily on LP pool health.

- The claims framework is still in development.

- Lacks extensive third-party audits.

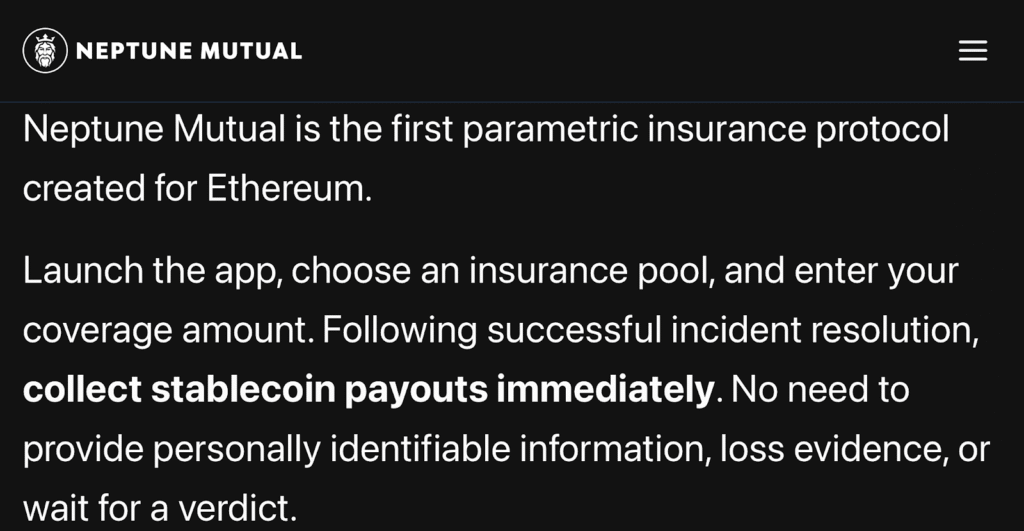

4. Neptune Mutual

(Source: Neptune Mutual website)

Neptune Mutual follows a parametric insurance model. It offers tailored coverage for exchange and protocol failures with automatic payouts based on predefined triggers.

Pros

- Fast, automated payouts eliminate delays.

- Clear rules on when and how claims pay out.

- Simple and transparent product design.

- No voting required by members.

- Focused on key high-risk areas like exchanges.

Cons

- Limited capital compared to major protocols.

- Parametric triggers may not fit every scenario.

- Untested during large-scale incidents.

- Narrower coverage scope.

- Still developing governance structure.

5. Sherlock Protocol

(Source: Sherlock Protocol website)

Sherlock Protocol offers insurance backed by professional security audits. It assesses covered protocols with assigned risk scores and sets premiums accordingly.

Pros

- Premiums linked to actual audit results.

- Experts assess protocol safety.

- High security standards across coverage.

- Vetted protocols only.

- Transparent risk framework.

Cons

- Narrow focus on audit-backed protocols.

- Coverage capacity may be limited.

- Heavy reliance on audit accuracy.

- Governance and claims process are still evolving.

- May not cover general DeFi risks.

6. Etherisc

Etherisc started in 2017, catering to parametric real-world insurance cases like flight delays and crop insurance. It uses a modular framework for custom products.

Pros

- Flexible open-source framework.

- Real-world parametric pilots show practical use.

- No single point of failure via modules.

- Community-led governance model.

- Focus on humanitarian and emerging market needs.

Cons

- Limited on-chain DeFi coverage.

- Oracle dependence adds risk.

- Governance and product refinement are ongoing.

- Smaller capital reserves.

- Less mainstream adoption for DeFi use.

7. NSure Network

(Source: NSure Network website)

NSure Network runs a decentralized insurance marketplace using dynamic pricing and prediction-market-style underwriting. It covers DeFi protocols, stablecoins, and staking risks.

Pros

- Marketplace offers flexible options.

- Price discovery aligns supply and demand.

- Token staking builds incentive alignment.

- Broad scope including stablecoins and staking.

- Governance is rewarded through token engagement.

Cons

- Still in development and testing.

- Adoption is limited so far.

- The claims process hasn’t been fully validated.

- Dependent on accurate risk models.

- Limited historical data for performance.

Emerging and Niche Players to Watch

Apart from the major platforms, a new wave of decentralised insurance projects is quietly gaining ground.

1. Unslashed Finance

Unslashed Finance specializes in real-time DeFi insurance with a capital-efficient model. It covers risks like exchange hacks, oracle failures, and validator slashing. The protocol automates payouts and allows liquidity providers to earn yields while supporting ecosystem security.

Pros

- Payouts happen automatically and transparently on-chain.

- Capital efficiency can reduce premiums.

- Supports a wide set of risks hacks, slashing, and oracle failures.

- Aims to serve both retail and institutional users.

- Automated claims avoid long voting delays.

Cons

- Still building market adoption, so coverage options may be limited.

- Total value locked remains small compared to major platforms.

- Coverage reliability depends on accurate oracles.

- Fewer proof points from past claim cycles.

- Risk pools need more depth for large-scale protection.

2. Bridge Mutual

Bridge Mutual is a permissionless, DAO-managed coverage platform. It offers flexible insurance for stablecoins, exchanges, and smart contract failures, with users staking stablecoins to underwrite policies.

Pros

- Permissionless underwriting means anyone can stake to earn.

- Covers popular assets stablecoins, exchanges, and protocols.

- Cross-chain expansion is underway into chains like BSC and Polygon.

- DAO governance lets users vote on policies and payouts.

- Reinsurance pools and yield strategies add financial depth.

Cons

- Claims depend on community vote, which can be slow.

- New protocol versions may introduce risk during transitions.

- Liquidity may be limited during large incidents.

- Complex vault structures may confuse new users.

- Still building trust compared to longstanding competitors.

3. Solace

Solace launched in 2020 as a DAO-driven protocol offering pay-as-you-go coverage. It provides dynamic portfolio protection with premiums calculated in real time. It’s available across Ethereum, Polygon, Aurora, and Fantom.

Pros

- The dynamic risk engine sets fair, real-time pricing.

- Portfolio-level coverage saves users from buying multiple policies.

- DAO governance means decisions are community-driven.

- Multi-chain support widens access.

- Adaptive to new risk categories as DeFi evolves.

Cons

- The claims outcome depends on DAO voting.

- Users need to stake tokens for full protocol participation.

- Still expanding its coverage catalog.

- Liquidity may be lower than legacy platforms.

- Governance outcomes can vary based on voter turnout.

Why Decentralized Insurance Matters in Web3

This section looks at why decentralized insurance is becoming essential infrastructure for a secure and reliable Web3 ecosystem.

1. DeFi and Smart Contracts are Exposed to Constant Risk

Web3 depends on smart contracts to run everything from lending protocols to NFT platforms. These contracts are written in code, and if that code has a flaw, it can be exploited. Hacks have drained billions from DeFi protocols, sometimes within minutes.

Traditional insurance providers don’t cover these kinds of risks, which leaves users with no safety net. That’s where decentralized insurance steps in. It offers specific coverage for smart contract failures and exploits.

Projects like InsurAce and Nexus Mutual give users the option to protect their funds against this type of loss, which adds an extra layer of security to using DeFi platforms.

2. Centralized Platforms Can Fail Without Warning

Many people use centralized exchanges and custodians to store or trade their crypto. When these platforms go down or freeze withdrawals, like FTX did, users can lose everything. Decentralized insurance helps cover that risk.

It creates policies that activate if a centralized exchange goes insolvent or halts user access. Since these policies are managed on-chain, users don’t need to depend on a single company’s promise.

Instead, they rely on a smart contract or community vote to determine a fair outcome. That gives users more confidence to hold or trade assets across different platforms.

3. Stablecoins Are Not Always Stable

Stablecoins are meant to hold a fixed value, but they can lose their peg. When TerraUSD collapsed, it wiped out billions and caused a ripple effect across crypto markets. Decentralized insurance can protect users when a stablecoin drops in value or fails completely.

Protocols like Risk Harbor have created coverage that triggers automatically if a stablecoin trades below its peg for too long. This kind of protection helps users manage risk when they hold or use stablecoins in DeFi strategies.

4. DAOs And Treasuries Need Protection Too

Web3 isn’t just about individuals. DAOs manage large treasuries and often hold millions in digital assets. These funds are exposed to the same risks as individual users, and in some cases even more. If a DAO uses a DeFi protocol that gets hacked, it could lose its entire treasury.

Decentralized insurance allows DAOs to buy coverage for the assets they manage. This gives them a way to protect their community’s resources and reduce the chance of total loss. It also shows members that risk is being taken seriously.

5. Traditional Insurance Can’t Keep Up With Crypto

Most traditional insurance companies are not set up to understand or underwrite blockchain-based risks. They move slowly, rely on paperwork, and often avoid anything they don’t fully control.

Decentralized insurance fills that gap. It is built by and for people who use Web3 tools every day. Policies can be created quickly, priced based on smart contract activity, and managed by decentralized communities.

This model matches the speed and structure of Web3, making it a better fit for users who want insurance without waiting on outdated systems.

“The decentralized insurance market size will grow from $2.36 billion in 2024 to $3.51 billion in 2025 at a CAGR of 48.7 %”

Evaluation Criteria for Ranking Projects

Before ranking the top platforms, it’s important to define what makes a project useful, reliable, and worth your trust.

1. Claims Process and Transparency Matter Most

The way a project handles claims is one of the most important things to look at. Some use community voting through a DAO to decide if a claim is valid, while others rely on smart contracts to automate the whole process.

Nexus Mutual uses a member voting system where people review each case before deciding. Risk Harbor takes a different approach and removes voting entirely by using a parametric model that automatically triggers payouts based on predefined conditions.

A good claims process should be fair, easy to understand, and give users clear steps for submitting and tracking their claims.

2. Capital Efficiency Shows How Well a Project Manages Risk

Every insurance platform needs capital to cover payouts. The way a project pools, invests, or allocates that capital affects how sustainable it is. InsurAce uses a portfolio-based model that spreads risk across different assets and chains, which helps manage liquidity.

Projects like Uno Re let you stake capital into specific risk pools, so capital is tied directly to coverage.

Efficient capital use means lower premiums for users and stronger protection during market volatility. It also reduces the risk of underfunded claims, which is a common problem in newer protocols.

3. Tokenomics Affects Incentives and Participation

A decentralized insurance protocol usually runs on a native token. That token is often used for staking, voting, or rewarding users who provide liquidity.

The way tokens are distributed, used, and governed plays a major role in how stable the system is. Nexus Mutual uses the NXM token, which members must stake to back insurance covers. This links financial risk to decision-making.

On the other hand, platforms like Tidal Finance use flexible token models to encourage growth across different chains. Strong tokenomics help align user behavior with the protocol’s long-term goals and ensure the system stays balanced.

4. Security practices and audits protect users

Smart contracts are the foundation of decentralized insurance, so the quality of those contracts is critical. A project that runs without regular audits or ignores security flaws puts users at risk.

Sherlock Protocol brings in third-party auditors to review every protocol it covers and uses those reports to help set premium prices. Most top platforms publish their audit results and share detailed risk frameworks.

Strong security practices include not just code reviews but also how the team responds to bugs, how quickly they patch issues, and how open they are about risks.

5. The governance structure shows how decisions are made

Since most decentralized insurance platforms are governed by DAOs, it’s important to understand how those DAOs work. Some give more control to token holders, while others use smaller councils or committees to manage decisions.

InsurAce and Etherisc allow token holders to vote on claims, fee structures, and new coverage products. Good governance means users can trust that decisions are made in the open, with clear rules and processes.

It also helps protect the protocol from manipulation or central control, which is especially important when real money is on the line.

Key Use Cases Driving Growth

These are the key areas where decentralised insurance is proving useful and driving new demand.

Smart contract failure protection is becoming standard

One of the biggest drivers of growth in decentralized insurance is the need for smart contract coverage. As more protocols are built on-chain, even the smallest coding error can lead to major losses.

We’ve already seen incidents like the bZx and Yam Finance exploits where bugs drained millions. DeFi users are starting to see coverage as a basic layer of risk management, especially when interacting with new or unaudited protocols.

Insurance platforms are responding with flexible products that cover bugs, logic errors, or unexpected interactions in smart contracts.

This demand is also growing among developers and DAOs who want to build user trust. Covering their own protocols makes them more attractive to users and investors.

Sherlock Protocol and InsurAce are already working directly with protocols to offer baked-in protection.

For many projects, this kind of insurance has become part of the launch checklist. It’s now seen less as an extra and more as a necessary step to operate in DeFi.

Stablecoin depegging coverage is growing fast

With the rise of algorithmic and asset-backed stablecoins, there’s a real need to protect against price instability. Stablecoin depegging has caused panic in markets, especially after the collapse of UST and smaller events around USDC and DAI.

When a stablecoin drops below its target value, users risk heavy losses. Insurance platforms have started offering depeg protection that automatically pays out when a coin trades below its peg for a set period.

This coverage helps keep confidence in stablecoins and gives traders and protocols a safety net. InsurAce was among the first to offer depeg protection for USDT, USDC, DAI, and BUSD.

Neptune Mutual and Bridge Mutual are now building similar tools. As stablecoins power much of the liquidity in DeFi, this use case has become one of the most requested.

DAO treasuries are insuring on-chain assets

DAOs manage large treasuries and hold assets across wallets, protocols, and chains. This exposure makes them vulnerable to smart contract risk, token volatility, and cross-chain bridge exploits.

Many DAOs are now buying insurance as part of their treasury strategy to protect funds from technical or market events. They’re treating risk protection the same way traditional companies manage balance sheet exposure.

Projects like Nexus Mutual and Unslashed Finance have started working directly with DAOs to offer custom policies for treasury assets.

The goal is to reduce risk while maintaining full control of assets on-chain. As DAOs grow larger and more professional, this kind of coverage is becoming a core part of treasury management.

CeFi exchange risk is still a concern

Despite DeFi growth, many users still hold assets on centralized exchanges. The collapse of FTX, hacks on KuCoin, and other incidents have shown how fragile these platforms can be.

Decentralized insurance is now offering exchange protection to cover losses from custody breaches or withdrawal freezes. These are events where users lose access to funds not because of bad trades, but because the platform itself fails.

Bridge Mutual and Neptune Mutual are leading this use case with parametric products that trigger payouts based on specific events like exchange downtime or insolvency reports.

Coverage like this is helping users hold exchanges more accountable and giving them options to manage risks that were previously unavoidable.

Yield farming and LP staking protection are on the rise

Yield farming has become a major activity in DeFi, but it comes with its own set of risks like impermanent loss, protocol failure, or liquidity pool exploits. As users chase higher returns across new pools and farms, they’re also looking for ways to protect their staked assets. This is where insurance products for LPs and yield farmers come in.

Projects like Tidal Finance and Solace are building tailored policies for users participating in high-risk DeFi strategies. These include flexible products that activate when pools are drained or platforms fail. With more complex strategies being offered, this kind of protection is starting to feel necessary, not optional.

For yield farmers, being insured means being able to farm without constantly worrying about whether a platform might disappear overnight.

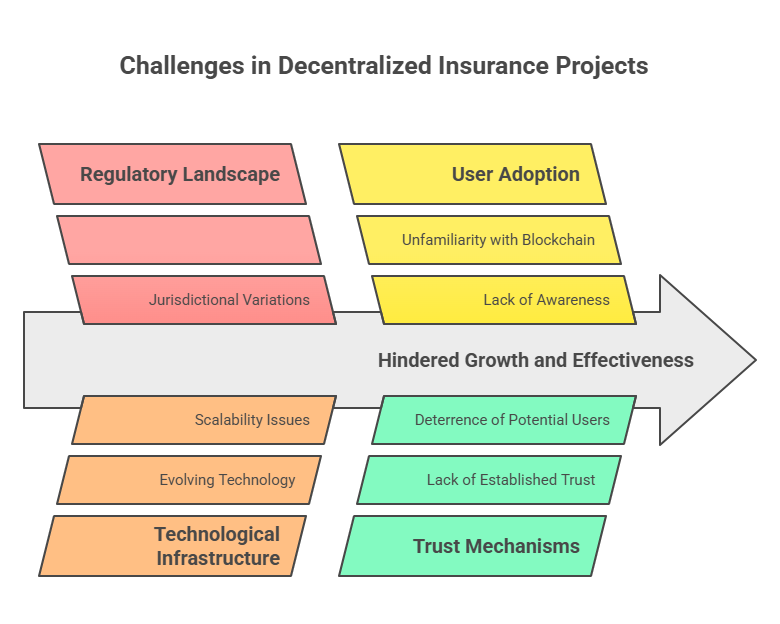

Challenges and Limitations Of Decentralized Insurance Projects

Even with growing adoption, decentralised insurance still faces serious gaps that slow down trust and scale.

Claims processing is still inconsistent

One of the biggest challenges in decentralized insurance is how claims are handled. In many protocols, users have to submit claims that are then reviewed or voted on by a group of token holders. While this sounds fair in theory, in practice, it can create delays and disputes.

Voters may lack the technical understanding needed to judge a claim or may simply vote in a way that protects their own interests. This makes the claims process unpredictable and sometimes frustrating for users.

Some platforms like Nexus Mutual use member voting, while others like Neptune Mutual rely on parametric triggers. Parametric systems remove the need for voting by using preset conditions, but they only work for specific types of events.

There’s still no universal standard, and different platforms are trying different models. Until this improves, claims processing will remain a sticking point that limits broader adoption.

Liquidity is limited and fragmented

Decentralized insurance platforms need capital to back policies and pay out claims. This capital comes from users who stake tokens or provide liquidity. The problem is that liquidity is spread thin across many projects and not all pools are well funded.

If a large claim happens, some platforms might not be able to pay it out fully or quickly. That risk discourages more people from buying policies or providing capital.

For example, newer protocols like Solace or NSure often have smaller capital reserves compared to more established ones like Nexus Mutual.

Even platforms with strong tech sometimes struggle to attract enough liquidity to offer meaningful coverage. Without deeper pools, platforms can’t grow their coverage or handle multiple large claims at once.

Regulation and legal uncertainty are major risks

Because decentralized insurance operates on-chain and often without formal legal structures, it exists in a grey area in many countries. Some regulators may see it as financial activity that requires licenses.

Others may treat it like a mutual fund or a cooperative. The lack of legal clarity makes it hard for these platforms to scale globally or serve users in more tightly regulated markets.

For instance, Nexus Mutual has a legal wrapper in the UK and requires KYC for that reason. Other platforms that skip KYC may avoid legal risk in the short term but face challenges if regulators decide to crack down.

There’s also the question of enforceability. If a protocol fails to pay a claim, there’s no legal recourse because it operates without a traditional company structure.

Pricing and underwriting models are still evolving

Traditional insurance relies on years of data to calculate risk and set prices. DeFi insurance does not have that luxury. Many projects are still figuring out how to price risk in an environment that changes fast. Some use historical exploit data, others rely on audits or community votes.

But none of these approaches is consistent yet. That means users might be paying too much for low-risk coverage or too little for high-risk exposure.

Sherlock Protocol tries to solve this by tying prices to audit scores, and InsurAce uses supply and demand to adjust premiums. Still, without standard metrics, it’s hard to compare products or know if a premium is fair.

This affects both buyers and liquidity providers who need accurate risk pricing to earn sustainable returns.

User education and product complexity slow adoption

Even in 2025, many DeFi users don’t fully understand how decentralized insurance works. The idea of staking to provide coverage or buying protection on a liquidity pool is not as intuitive as traditional insurance.

Add to that the technical interfaces, governance models, and token mechanics, and many users feel overwhelmed. As a result, they avoid the product altogether or stick with uninsured strategies.

Platforms like Etherisc and Bridge Mutual are trying to simplify interfaces and explain their products better, but it’s still early. Most users aren’t familiar with risk scoring, policy limits, or parametric triggers.

Until insurance becomes easier to understand and use, growth will remain limited to more experienced parts of the DeFi community.

The Future of Decentralized Insurance

Decentralised insurance is developing fast, and what comes next could shape how Web3 handles risk at scale.

Advanced risk analytics and AI-powered underwriting

In the next wave of decentralized insurance projects, AI and data tools will play a vital role. These platforms will use smart contracts alongside machine learning and real-time risk feeds from oracles.

That means risk assessments and premium prices will adjust based on current market and protocol data. It helps create fairer pricing and reduces the chance for mispriced or underfunded coverage.

Parametric models will gain wider use

Parametric insurance where payouts trigger automatically when certain benchmarks are met is already expanding beyond flight delays and crop protection.

As more blockchain oracles become trusted and real-world sensors join data feeds, this method will be used for more smart contract events, market drops, and staking slashing events. That means faster and more reliable claims without waiting for votes or audits .

Cross-chain coverage and interoperable risk pools

As DeFi spreads across different chains, insurance platforms will need to follow. Future projects will build risk pools that span Ethereum, BNB Chain, Solana, Avalanche, and others.

This interoperability helps insurers reduce capital fragmentation and offer broader protection for users who work with multiple chains and bridges .

On-chain reputation and tokenized risk markets

Users and protocols will increasingly build digital reputations on-chain based on activity, claims history, and risk scores. These reputations link to tokenized risk shares that can be bought, sold, or staked.

This opens the door to secondary markets for insurance risk, giving providers new ways to manage exposure and letting users invest in underwriting.

Regulatory clarity and collaboration with TradFi

Regulators and traditional insurers are already exploring blockchain-native insurance. Expect clearer frameworks and licensing over the next few years. Some projects are already working under legal wrappers or with established insurers to comply with regional rules.

This aligns decentralized protocols with real-world governance and opens the door to institutional capital and mainstream trust.

Conclusion

Decentralised insurance is becoming a main part of how people manage risk in crypto and DeFi. As the space grows, so does the need for protection against smart contract failures, stablecoin depegs, exchange collapses, and other technical risks. The platforms leading the charge are building real tools that give users more control and confidence in how they protect their assets on-chain.

Whether you’re a DAO managing a treasury, a yield farmer staking in new pools, or a trader holding assets across multiple chains, there’s now a range of insurance options that are flexible, transparent, and accessible.

The best decentralised insurance project is the one that fits your risk profile and offers fair pricing, a proven claims process, and strong liquidity.

Frequently Asked Questions

Is decentralised insurance safe to use?

Yes, decentralised insurance is generally safe when used with trusted platforms that have a strong track record and transparent claim systems.

Can I earn rewards by providing liquidity to a decentralised insurance protocol?

Yes, most decentralised insurance projects allow users to stake or provide capital in return for yield or rewards, based on the risk pool’s performance.

What makes a decentralised insurance project trustworthy?

A decentralised insurance project is trustworthy when it has clear claims processes, enough liquidity to cover payouts, strong security audits, and a transparent governance model.

Is KYC required to use the best decentralised insurance project?

No, not all decentralised insurance platforms require KYC, though some like Nexus Mutual may ask for it due to legal structures in certain jurisdictions.

Which decentralised insurance projects offer stablecoin depeg coverage?

Stablecoin depeg coverage is offered by platforms like InsurAce, Neptune Mutual, and Bridge Mutual for assets like USDT, USDC, and DAI.

How are claims processed in decentralised insurance platforms?

Claims are processed through either on-chain governance voting or automated parametric triggers, depending on the platform’s model.

Can decentralised insurance cover DAO treasury funds?

Yes, many decentralised insurance projects now offer customised coverage for DAOs looking to protect treasury funds from on-chain risks.

What are the benefits of using the best decentralised insurance project?

The benefits include protection from common DeFi risks, automated payouts, on-chain transparency, and the ability to earn by participating in risk pools.