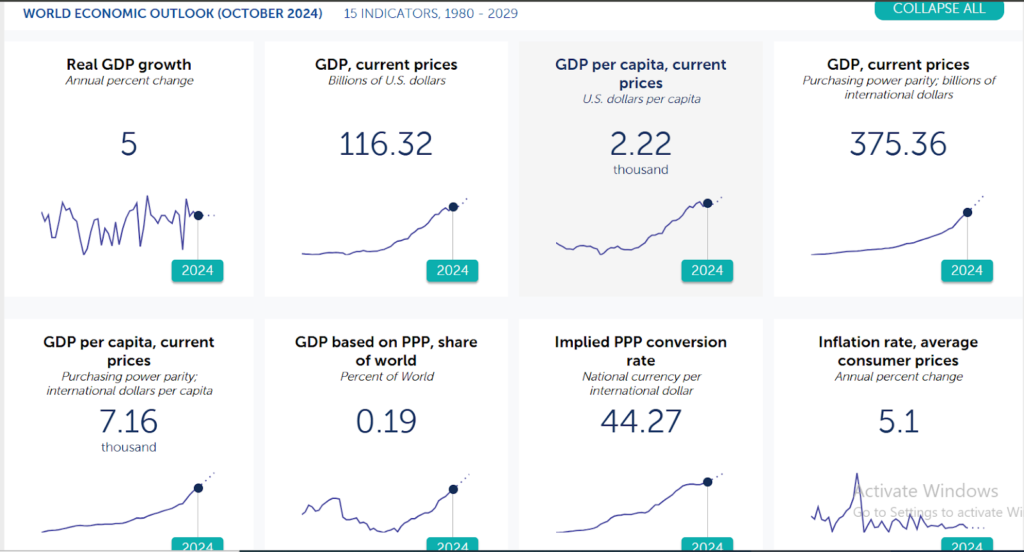

Current Economic Situation in Kenya

Source: IMF DataMapper

Despite being the largest economy in East Africa, Kenya has faced and is still facing several challenges that are consequently detrimental to the economy. These challenges range from climate risks affecting agriculture to global economic shifts.

However, Kenya’s resilience is evident. In late 2025, the Central Bank of Kenya lowered its benchmark rate to 9% to stimulate credit growth and support economic activity.

The country maintained steady growth, with projections of 5.2% for 2025, driven by a recovering agricultural sector and stable energy costs. Inflation remained moderate at 4.5% in November 2025, sitting comfortably within the government’s target band.

The Kenya Vision 2030 remains the central development blueprint, aiming to transform Kenya into a newly industrializing, middle-income country. The World Bank Group continues to support this vision, aligning its strategies with Kenya’s focus on the digital economy and human capital.

The official website of the Kenya Vision 2030 writes on the vision thus:

A national long-term development blueprint to create a globally competitive and prosperous nation with a high quality of life by 2030, that aims to transform Kenya into a newly industrializing, middle-income country providing a high quality of life to all its citizens by 2030 in a clean and secure environment.

Kenya has been innovative in growing its economy by diversifying its revenue sources. Beyond traditional sectors like tourism and agriculture, the innovation-driven economy stands to gain immensely from blockchain adoption, particularly in financial inclusion and the transparency of agricultural exports.

The World Bank Group (WBG) is also highly invested in the success of Kenya’s national reformation plan. In November 2022, a framework was designed by the Fiscal Year (FY)2023-2028 Country Partnership Framework (CPF) in alignment with five major provisions.

The CPF drew from the WBG’s Country Partnership Strategy (CPS) FY14-FY20 for Kenya, lessons from the CPS Completion and Learning Review (FY22), the FY20 Systematic Country Diagnostic, a Country Private Sector Diagnostic (FY19), over 34 stakeholder consultations, and is aligned to the Kenya Vision 2030. It also aligns directly with the World Bank’s Africa Strategy, focused on jobs and economic transformation, digital economy, human capital, universal access to electricity, climate change mitigation and adaptation, addressing fragility, conflict, and violence, and achieving gender equality.

In the course of the implementation of this World Bank strategy, up to $10.17 billion has been invested in Kenya, through the International Finance Corporation (IFC), the International Bank for Reconstruction and Development (IBRD), the Multilateral Investment Guarantee Agency (MIGA), as well as the International Development Association (IDA).

Crypto Law in Kenya

Source: Freeman Law

The regulatory environment for cryptocurrency in Kenya underwent a historic transformation with the passage of the Virtual Asset Service Providers Act, 2025. This Act supersedes previous ambiguity, creating a clear “same activity, same risk, same regulation” approach.

Prior to this Act, the Central Bank of Kenya (CBK) had issued warnings regarding volatility. However, the VASP Act represents a shift from caution to regulation, establishing a structured environment that supports responsible innovation and investor confidence.

The Virtual Asset Service Providers Act, 2025 This landmark legislation serves as the primary legal framework. Key provisions include:

- Licensing: It mandates the licensing of exchanges, custodial wallets, and brokers through the Capital Markets Authority (CMA).

- Consumer Protection: It introduces a Consumer Protection Code to handle dispute resolution and ensure transparency for users.

- Innovation: It creates a regulatory sandbox to foster the development of innovative blockchain products within a controlled environment.

- Compliance: Licensees must establish Anti-Money Laundering (AML) and Counter-Terrorism Financing (CFT) obligations consistent with national laws.

The Act distinguishes between regulated “virtual assets” and “digital representations of fiat currencies” (like CBDCs) or “closed ecosystem” tokens, which may fall under different or no regulation depending on their use.

Other relevant regulations include the Finance Act, 2025, which codified the taxation of digital assets, and the Computer Misuse and Cybercrimes Act, which prescribes cybersecurity measures for VASP licensees.

Current State of Crypto Adoption in Kenya

Source: CoinGecko

The Kenyan cryptocurrency market has evolved into a vibrant ecosystem supported by regulatory maturity. In 2025, the projected revenue in the market is US$108.6 million. While earlier years saw varying estimates of ownership, current data projects the number of users to reach 1.39 million by 2026, with a user penetration rate of 2.25% in 2025.

Kenya’s growing tech-savvy population and mobile money ecosystem have fueled this surge. The market is characterizing by several dynamic trends:

- Remittances: Kenyans are increasingly using blockchain for lower-cost cross-border transfers, which outperform conventional banking speed and pricing.

- DeFi and Tokenization: There is growing participation in Decentralized Finance (DeFi) for lending and yield farming. Furthermore, real-world assets like real estate and carbon credits are being tokenized into tradable blockchain assets.

- Trading: Platforms such as Binance, Yellow Card, and local startups continue to attract participation, now operating under the new licensing requirements.

The Kenyan cryptocurrency market has consistently grown since its government’s public warnings on the state of the ecosystem in 2015. As at July 2023, Kenya was recognized by Forbes as one of the top five crypto owning countries in Africa, with a trading volume of about $18.6 billion from at least 8% of the country’s population.

In the world, cryptocurrency is most popular among people below 35 years. Therefore, Kenya’s current population of 80% youth proves the country a fertile ground for cryptocurrency. Further evidence of this is Kenya’s 15th place as CoinGecko’s most curious country about crypto. Also called “Silicon Savannah” (nicknamed after the Silicon Valley), Kenya’s technology ecosystem is booming and cryptocurrency is a huge part of this.

Kenyans have adopted a robust utility approach towards cryptocurrencies, viewing them beyond digital assets for investment purposes. Crypto has been incorporated into companies such as AZA Finance that allow businesses make or receive international payments at a cheaper rate, Fonbnk that allows users exchange airtime for crypto, and Grassroot Economics that drives community inclusion through crypto. These, in addition to more popular peer-to-peer exchanges like Binance, have contributed to spurring Kenyan’s attraction to the blockchain ecosystem.

Factors Affecting Adoption of Crypto in Kenya

Source: Nairametrics

Regulatory Clarity vs. Complexity

The implementation of the VASP Act in 2025 has eliminated much of the previous legal grey area, which is a significant driver for institutional interest. However, challenges remain, including some persisting overlap between the oversight of the Central Bank of Kenya (CBK) and the Capital Markets Authority (CMA).

Taxation

The new tax regime is a critical factor influencing user behavior. The Finance Act 2025 introduced specific levies:

- Capital Gains Tax (CGT): Disposals of crypto assets now attract a 15% tax on net gains.

- Excise Duty: A 10% excise duty is applied to service charges by exchanges and wallet providers.

- Compliance: VASPs are required to remit this duty monthly to the Kenya Revenue Authority (KRA), and traders are advised to maintain detailed transaction logs.

Security and Fraud Risks

Despite regulation, cybersecurity remains a concern. Exchanges face risks of attacks, and public scams (Ponzi schemes) continue to target uninformed users. The new Act addresses this by requiring licensees to meet prescribed cybersecurity measures and maintain physical presence for accountability.

Market Volatility

Drastic price swings continue to discourage conservative investors, highlighting the need for the stable policy environment that the new Act aims to provide.

Conclusion

Kenya’s government has transitioned from viewing cryptocurrencies with apprehension to establishing a robust legal framework that recognizes their economic potential. The enactment of the Virtual Asset Service Providers Act 2025 marks a pivotal moment, balancing innovation with consumer protection and financial stability.

Although the introduction of a 15% capital gains tax and 10% excise duty presents a new cost for users, it also signals the formal integration of crypto assets into the national economy. The sector is poised for steady growth, with revenues projected to rise to US$110.4 million by 2026.

To fully realize the goals of Vision 2030, Kenya must continue to refine these regulations, ensuring they foster financial inclusion and attract foreign investment while safeguarding users against the inherent risks of the digital asset market