Money as a medium of exchange has changed a lot over time, starting with things like shells moving to fabrics, precious metals, paper notes, cash, and now cryptocurrency. Although cryptocurrency remains mostly unregulated, the arrival of Central Bank Digital Currencies (CBDCs) marks the start of a new chapter in the history of money.

The Central Bank Digital Currencies (CBDCs) has become a hot topic in the financial market especially as more countries focus on digital versions of their national currencies. But what does this mean for the existing cryptocurrency landscape? Cryptocurrencies, like Bitcoin and Ethereum, were created to decentralize money and take leverage on the traditional financial systems.

CBDCs, on the other hand, are digital currencies that are fully controlled by central banks. As governments push forward with CBDCs, there are growing concerns on how this will affect cryptocurrencies, Such as if CBDCs will compete or complement crypto?

Key takeaway

- CBDCs can encourage more people to use digital currencies, making it easier for them to engage with both CBDCs and cryptocurrencies.

- The introduction of CBDCs may lead to clearer rules and regulations for cryptocurrencies, which can help protect investors and foster a safer trading environment.

- CBDCs could compete directly with cryptocurrencies, potentially influencing their popularity and market options value as people choose between state-backed and decentralized options

- CBDCs can change how central banks implement monetary policy, which might affect the overall demand and value of cryptocurrencies in the market.

“The rise of CBDCs may challenge the dominance of traditional cryptocurrencies.”

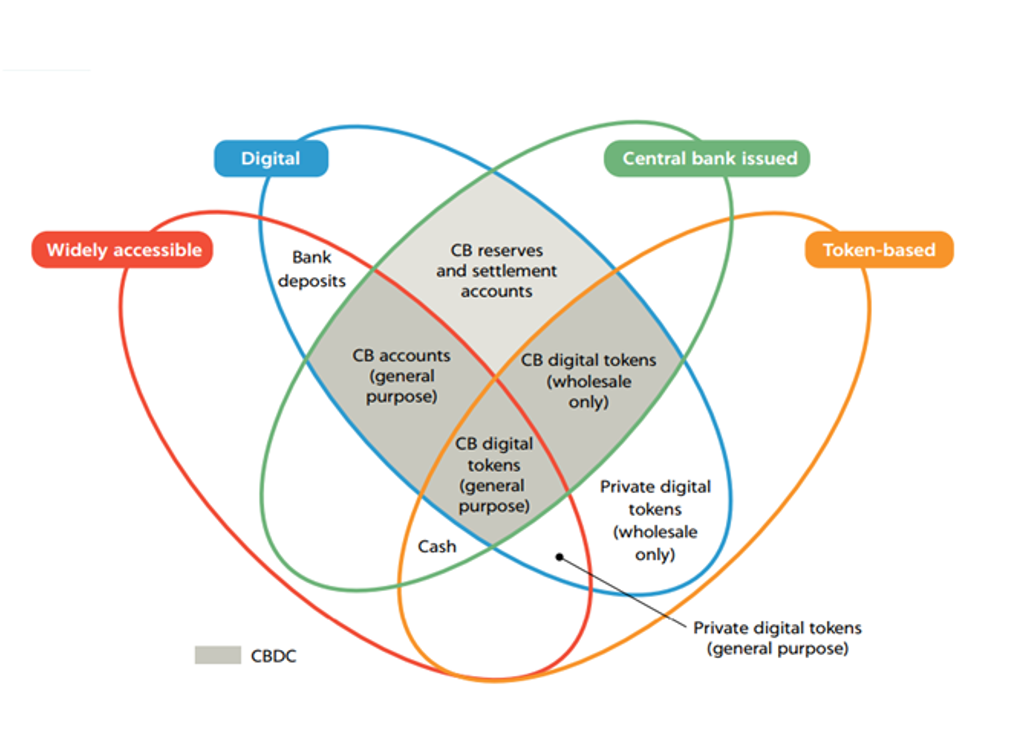

What are CBDCs

Source: CFTE

CBDCs are digital currencies issued by a nation’s central bank, designed to function like traditional money but in a digital format.

They are legal tender and are backed by the trust and authority of the government. CBDCs aim to improve financial systems by offering a secure, fast, and efficient way to carry out transactions, whether for everyday purchases or larger financial activities.

Central Bank Digital Currency (CBDC) is very important compared to regular cryptocurrencies and traditional money. It helps lower costs, stops fake money, and strengthens the value of official currency. It also makes the payment system more accessible to everyone.

How CBDCs Differ from Cryptocurrencies

Although both CBDCs and cryptocurrencies exist in digital form, there are significant differences between the two. The key distinction lies in control and regulation:

| CBDCs | Cryptocurrency | |

| Centralised Vs Decentralised | CBDCs are controlled by central banks, making them centralized, | Cryptocurrencies like Bitcoin are decentralized, meaning they operate without any central authority. |

| Stability | CBDCs are backed by the government, which gives them a stable value | Cryptocurrencies, on the other hand, can be highly volatile due to market speculation. |

| Legal Status | CBDCs are considered legal tender, meaning they must be accepted for transactions in the issuing country. | Cryptocurrencies, however, are often not recognized as official currency in many places. |

Types of CBDCs (Retail vs. Wholesale)

Retail CBDCs are designed for the general public. These are digital currencies that individuals and businesses can use for everyday transactions, just like cash or credit cards. The goal is to provide an easy and secure way for people to pay for goods and services digitally. Retail CBDCs, or digital currencies can be set up in three main ways: direct, indirect, and hybrid.

- Direct Model

In this model, people can deposit their money straight into accounts with the central bank. This makes it accessible for everyone—from local businesses to freelance workers. - Indirect Model

Here, commercial banks handle CBDC accounts or wallets for customers. This approach keeps existing banking services in place, so the central bank doesn’t need to manage customer accounts directly. - Hybrid Model

With the hybrid model, customers don’t have accounts with the central bank. Instead, they use third-party providers, like e-money or payment service providers, to access their CBDCs.

Wholesale CBDCs are used primarily by financial institutions. These CBDCs are meant for large-scale transactions between banks or other financial entities. Wholesale CBDCs aim to make these transactions faster, more secure, and more efficient, improving the overall financial infrastructure.

Both types of CBDCs serve different purposes but together could help modernize the way money flows through economies, benefiting both individuals and institutions.

Examples of Countries with CBDC

Here’s a look at some countries using their own digital currencies:

Ukraine: E-hryvnia

The National Bank of Ukraine has been working on the e-hryvnia since 2018, conducting early tests with a small pilot in which 5,443 coins were issued for use by its employees. In September 2021, the bank launched a larger project to explore the digital hryvnia’s potential, with a full rollout expected by the end of 2024.

China: Digital Yuan (e-CNY)

Although China has banned cryptocurrencies, it’s a leader in developing CBDCs. The digital yuan, or e-CNY, has been tested since 2020 in cities like Shenzhen, Suzhou, and Beijing, allowing people to use it for payments and even government subsidies.

Bahamas: Sand Dollar

In October 2020, the Bahamas became the first country to officially launch a CBDC, the Sand Dollar. Created to boost financial inclusion, the Sand Dollar makes payments and transfers easier, especially in remote areas across the islands.

Sweden: E-krona

Sweden’s central bank, the Riksbank, is testing the e-krona to ensure stability in payments as cash use declines. The goal is to secure a reliable, accessible digital payment system for everyone.

Nigeria: eNaira

Nigeria introduced its CBDC, the eNaira, in October 2021 to support financial inclusion, speed up payments, and cut transaction costs. The eNaira is used for various payments, helping Nigeria’s digital economy grow.

Uruguay: Digital Peso

Uruguay was one of the first countries to experiment with a digital currency. Its Central Bank launched the digital peso pilot in 2017 to test how digital money could improve payments and support financial inclusion.

Benefits & Risks of CBDCs

Pros

- Increased Stability: CBDCs depend on the reliability of central banks, which helps reduce the risk from third parties and makes the financial system more stable.

- Lower Costs: By allowing central banks to interact directly with the public, CBDCs can help cut down on transaction costs, eliminating the need for costly banking systems.

- Greater Access: CBDCs can help more people access financial services, especially those who are currently underserved.

Cons

- Privacy Concerns: CBDCs require a lot of personal information, which raises privacy issues. Central banks would monitor for fraud, possibly allowing the government to access financial information without middlemen.

- Government Control: There’s a risk that governments could use CBDCs to influence how people spend their money. They might set rules on what can be purchased, which could limit personal financial freedom.

- Security Risks: Since CBDCs are controlled by central banks, this centralization could create security issues. A successful cyberattack could target this single point of control, potentially disrupting the entire economy.

“The future of finance may be a blend of CBDCs and cryptocurrencies.”

Why Are Central Banks Developing CBDCs?

Source: WhiteBIT

Central Bank Digital Currencies (CBDCs) have become a major focus for many countries worldwide. But why are central banks so keen to develop them? Several key factors are behind this trend, including the desire to improve financial inclusion, combat financial crime, enhance payment systems, and address geopolitical concerns.

Key Drivers Behind CBDC Adoption

Below are the key drivers behind CBDC adoption

Financial Inclusion

One of the main reasons central banks are developing CBDCs is to promote financial inclusion. Many people around the world, especially in developing countries, do not have access to traditional banking services.

By creating a digital currency directly backed by the central bank, governments hope to make it easier for everyone to access and use financial services, even in remote areas. This could help reduce poverty and improve economic opportunities for millions.

For instance In some countries where a large part of the population lives far from banks. People might spend hours traveling just to open a bank account or withdraw cash. With CBDC, they could use their mobile phones to store and send money right from their village. This could save time and make financial services available to more people.

Combating Financial Crime

CBDCs can also play a role in reducing financial crime. By using digital currencies that are fully traceable and monitored, central banks can better track illegal activities like money laundering, terrorism financing, and tax evasion.

Unlike cash, which can be hard to trace, digital currencies leave a clear record of every transaction, making it easier for authorities to spot suspicious activity and take action.

This can be done by CBDC by encrypting access to financial data while verifying that transactions are legal and trustworthy. With every transaction recorded on a central ledger, authorities can easily trace the flow of money, which is crucial in identifying suspicious activities.

Efficiency in Payment Systems

Another key driver is the push for more efficient payment systems. Current payment methods, especially cross-border transfers, can be slow and expensive. CBDCs can offer faster, cheaper, and more secure transactions, both within countries and across borders.

Cross-border payments, like sending money to families in other countries, are important for economic growth in today’s connected world. Right now, most people send money abroad using money transfer companies that rely on their own global networks. However, sending money internationally has some well-known problems.

First, fees are often high. Second, in some cases, there’s no guarantee the full amount will reach the person it’s meant for. Third, these payments face issues because different countries’ payment systems aren’t connected. Some of these issues could be solved by using Central Bank Digital Currencies (CBDCs).

The issuance and use of CBDCs for payment can potentially help simplify intermediation chains, increase speed, and lower cost. This could reduce costs for businesses and consumers while improving the overall economy. Digital currencies can also operate 24/7, unlike traditional banks, which often have limited hours and delays during holidays.

Geopolitical Motivations

Here are a few geopolitical consideration drivers behind CBDC adoption

Monetary Sovereignty and Global Competition

On a global scale, many countries are developing CBDCs to protect their monetary sovereignty and maintain control over their economies. As private cryptocurrencies like Bitcoin and stablecoins become more popular, central banks worry that they could lose control over their national currencies.

Issuing a central bank digital currency (CBDC) could help reduce the use of private digital currencies like Libra. A CBDC would create a new way to make digital payments and allow people to complete payments instantly, similar to what cash does today.

According to Doing He, modern policies, guided by committees and the independence of central banks, are important for keeping our currency stable. However, central banks still need to make their money appealing for people to use.

By creating a CBDC, a country can ensure that its currency remains relevant and prevent private companies or foreign currencies from dominating its economy.

Mitigating the Dominance of Private Cryptocurrencies

Another reason for developing CBDCs is to counter the rise of private cryptocurrencies. Cryptocurrencies like Bitcoin and Ethereum operate outside of government control, which poses a challenge for central banks.

By offering a government-backed alternative, central banks hope to reduce the influence of these private currencies and ensure that they can still manage monetary policy effectively. CBDCs can provide the same digital convenience that people seek in cryptocurrencies but with the added stability and trust that comes with central bank backing.

“CBDCs could provide stability in a volatile crypto market.”

How CBDCs Impact the Cryptocurrency System

Source: Youholder

The introduction of CBDCs could also affect how people adopt and use cryptocurrencies. Will CBDCs encourage more people to use digital currencies, or will they limit the growth of the crypto ecosystem?

CBDCs could drive crypto adoption by making people more comfortable with the idea of digital currencies. If governments push CBDCs, it might increase public trust in digital money overall, encouraging people to explore cryptocurrencies as well.

However, if CBDCs become dominant, they could also limit the need for cryptocurrencies in everyday transactions, especially in countries where people might prefer a government-backed currency over a decentralized one.

CBDCs vs. Cryptocurrencies: Competition or Coexistence?

It is believed that CBDCs will compete directly with cryptocurrencies by offering a government-backed digital alternative. Others think they can coexist, with each serving different purposes in the economy.

For example, CBDCs could be used for everyday payments because of their stability, while cryptocurrencies could remain popular for investments or innovative financial services. Here’s a simplified look at how CBDCs might affect the cryptocurrency market:

Increased Competition

CBDCs will introduce a government-backed alternative to cryptocurrencies. As a result, people and businesses might prefer using CBDCs due to their stability and backing by central banks.

This could lead to increased competition between CBDCs and cryptocurrencies, potentially reducing the demand for private digital currencies. However, cryptocurrencies are likely to maintain appeal for those seeking decentralized finance options.

Regulator Pressure

As CBDCs gain prominence, governments may impose stricter regulations on cryptocurrencies to encourage the use of their digital currencies. This could include tighter rules on cryptocurrency exchanges, taxes, and anti-money laundering (AML) requirements.

Such regulations might slow down the growth of some cryptocurrencies or push certain operations underground.

Enhanced Legitimacy for Digital Assets

The introduction of CBDCs could also benefit the broader digital asset space by normalizing the concept of digital currencies.

As more people become familiar with using digital money through CBDCs, they may be more inclined to use cryptocurrencies, thus broadening the market. It may also foster innovation, with central banks and private cryptocurrency developers pushing each other to create better technologies.

Financial Inclusion and Accessibility

CBDCs are designed to provide easier access to banking services, especially in regions where traditional banking is limited. This increased accessibility could extend to cryptocurrencies as well, as the infrastructure for digital finance improves. People with access to CBDCs might also focus on other digital assets, which could drive cryptocurrency adoption in underbanked areas.

Reduced Volatility

One of the key challenges in the cryptocurrency market is price volatility. CBDCs, being backed by governments, are expected to offer price stability, unlike volatile assets like Bitcoin.

As a result, some investors might choose to move their assets to CBDCs as a safer option. However, volatility also attracts traders looking for quick profits, meaning cryptocurrencies might still hold appeal for high-risk, high-reward trading.

Impact on Stablecoins

Stablecoins are cryptocurrencies pegged to traditional currencies, like the U.S. dollar, to reduce price swings. With CBDCs providing a government-backed stable alternative, the demand for stablecoins may decrease. However, stablecoins still offer advantages like operating on decentralized networks, which some users may prefer over government-controlled CBDCs.

Regulatory Implications for Stablecoins

One of the biggest areas where CBDCs could impact stablecoins is in regulation. Governments are likely to introduce stricter regulations for stablecoins if they also offer their own CBDCs.

This could make it harder for stablecoins to operate in some markets or require them to meet higher standards. On the other hand, clear regulations could also bring more legitimacy to the stablecoin market, making them more widely accepted.

“With CBDCs, central banks are saying yes to digital transformation.”

Impact of CBDCs on Cross-Border Transactions

Source:Fineksus

Disrupting the Remittance Market

Central Bank Digital Currencies (CBDCs) have the potential to shake up the remittance market, which allows people to send money across borders. Right now, many people use traditional remittance services like Western Union or newer crypto-based methods.

CBDCs could offer a government-backed digital option that might change how these transfers work, offering a safer and more controlled alternative.

Traditional Remittance vs Crypto vs CBDCs

Traditional remittance services are widely used but have some drawbacks. These include high fees, slow transfer times, and reliance on banks or third-party services. Crypto, on the other hand, offers faster transactions and lower costs but comes with risks such as volatility and a lack of regulation.

CBDCs could offer a middle ground, providing the safety of government-backed currencies with the speed and cost-effectiveness similar to crypto.

Faster, Cheaper Cross-Border Payments with CBDCs

CBDCs could make cross-border payments faster and cheaper by reducing the need for intermediaries. Instead of going through multiple banks or companies, CBDC payments could happen directly between central banks or individuals.

This could greatly reduce fees and time delays, making international transfers more efficient, especially for people in developing countries who rely on remittances.

How CBDCs Could Challenge Crypto-Powered Remittance Solutions

CBDCs pose a direct challenge to crypto-powered remittance solutions. Currently, cryptocurrencies like Bitcoin and stablecoins are used for remittances because they offer lower costs and faster transactions compared to traditional methods.

But CBDCs, if designed with global use in mind, could offer these same benefits while eliminating the risks tied to crypto’s volatility and regulatory uncertainty. Governments might also push CBDCs as a safer alternative, which could limit the use of cryptocurrencies in this space.

Use Cases of Crypto in Remittances

Cryptocurrencies have found an effective use in the remittance market, especially in regions where traditional banking services are limited or expensive. People often use crypto to send money home quickly and at a lower cost than traditional remittance services.

Stablecoins, which are pegged to fiat currencies, have become especially popular because they avoid the volatility seen with other cryptocurrencies like Bitcoin. These use cases have proven that crypto can make a big impact in the remittance space, providing both speed and cost savings.

Can CBDCs Match Crypto’s Efficiency in Remittances?

The big question is whether CBDCs can match the efficiency of cryptocurrencies in remittances. While CBDCs could offer fast and cheap cross-border payments, their success will depend on how they are implemented.

If CBDCs are widely accepted, easy to use, and integrated across borders, they could compete with or even surpass crypto in terms of efficiency. However, cryptocurrencies have a head start in this space, and it will take time for CBDCs to catch up, especially if there are delays in regulatory approval or technical hurdles.

“CBDCs could legitimize digital currencies in the eyes of the public.”

Regulatory Implications of CBDCs for Cryptocurrencies

Source:icrrd

As central banks around the world explore the development of their own digital currencies, known as Central Bank Digital Currencies (CBDCs), there are major changes underway that could reshape the regulatory landscape for cryptocurrencies. Let’s look at how CBDCs might affect crypto regulations and what this means for digital assets and decentralized finance.

The Role of Governments in Shaping Crypto Policy

Governments have always played a role in regulating money and finance, but the rise of cryptocurrencies introduced new challenges. As CBDCs become more popular, it’s likely that governments will step up their efforts to create clear rules for digital currencies and other crypto activities.

While the goal of these policies is often to protect users and prevent fraud, there’s also concern that strict policies could limit the freedoms that many in the crypto space value.

Stricter Regulatory Oversight Due to CBDCs

With CBDCs, governments can have complete control over the digital currency system, including who can access it, how it’s used, and how it’s tracked. This could lead to tighter regulations across the entire crypto market.

For example, many governments may start requiring stricter licensing for crypto exchanges and other platforms, along with more detailed reporting on crypto transactions. This kind of oversight could limit the ability of individuals to conduct transactions anonymously, as all activity on a CBDC platform is likely to be closely monitored.

Privacy and Anonymity Concerns in a CBDC-Driven World

CBDCs offer governments greater oversight, but they also raise privacy concerns. With CBDCs, every transaction can be tracked, which means there may be less room for anonymous transactions in the financial system.

While CBDCs could make it easier to fight financial crimes, they could also make it harder for people to maintain privacy. For many in the crypto community, privacy is a key part of why they use cryptocurrencies, so the rise of CBDCs and the possible reduction of anonymous options could become a major point of debate.

Effects on Decentralized Finance (DeFi)

Decentralized Finance, or DeFi, is a part of the crypto world that aims to provide financial services without the need for banks or other middlemen. DeFi platforms are built on public blockchains and use smart contracts to carry out financial transactions automatically.

However, with CBDCs entering the picture, there could be significant changes to how DeFi is allowed to operate.

Will CBDCs Restrict the Growth of DeFi?

CBDCs are controlled by central banks, which could mean more rules for DeFi platforms. Some governments might see DeFi as a competitor to traditional banking and the control offered by a CBDC.

As a result, they may introduce policies that make it harder for DeFi projects to operate freely. For example, some DeFi platforms could face restrictions on the kinds of financial products they can offer, making it difficult for them to compete with traditional financial systems.

Regulatory Frameworks Impacting DeFi Innovation

The impact of CBDCs on DeFi may go beyond restrictions and directly affect innovation. With stricter regulatory frameworks, DeFi platforms may have to invest more resources in compliance, which could slow down the development of new ideas and projects.

For instance, if DeFi platforms are required to follow the same reporting standards as banks, this could place a burden on smaller DeFi projects that may lack the resources to meet these requirements. In the long run, such regulations could stifle innovation in the DeFi space, limiting the development of new financial tools and options.

CBDCs are likely to bring new regulations and oversight that could affect the broader cryptocurrency market, including both traditional cryptocurrencies and DeFi. While the impact of these changes is yet to be fully understood, the push for a regulated digital economy suggests that the landscape of cryptocurrencies and DeFi could shift significantly in the coming years.

Conclusion

The introduction of CBDCs will undoubtedly reshape the financial landscape, presenting both challenges and opportunities for the cryptocurrency market. While CBDCs will bring increased competition and regulatory scrutiny, they could also legitimize digital currencies and create more awareness of the broader crypto space.

Ultimately, both CBDCs and cryptocurrencies are likely to coexist, serving different purposes for various types of users.

FAQs

What are Central Bank Digital Currencies (CBDCs)?

CBDCs are digital forms of a country’s official currency issued and regulated by the central bank. Unlike cryptocurrencies, which are decentralized, CBDCs are centralized and designed to maintain the stability of the national economy.

How might CBDCs affect the value of cryptocurrencies?

CBDCs could impact cryptocurrency values by providing a stable digital currency option. If people prefer the security and trust of CBDCs, it might reduce demand for some cryptocurrencies, potentially lowering their value.

Will CBDCs compete with cryptocurrencies?

Yes, CBDCs may compete with cryptocurrencies. While CBDCs are backed by governments and offer stability, cryptocurrencies provide more freedom and innovation. The competition will depend on user preferences and how well each meets people’s needs.

What benefits could CBDCs bring to the cryptocurrency market?

CBDCs could bring benefits like increased legitimacy and acceptance of digital currencies. As more people become familiar with CBDCs, they may also become more open to exploring cryptocurrencies, leading to greater adoption in the long run.

Can CBDCs and cryptocurrencies coexist?

Yes, CBDCs and cryptocurrencies can coexist. Each serves different purposes; CBDCs aim for stability and trust, while cryptocurrencies focus on decentralization and innovation. Together, they can enhance the digital financial ecosystem.